All Categories

Featured

Table of Contents

If you pick degree term life insurance, you can spending plan for your premiums since they'll stay the same throughout your term. And also, you'll recognize precisely just how much of a death advantage your recipients will receive if you pass away, as this amount won't change either. The rates for level term life insurance policy will certainly depend upon numerous factors, like your age, health and wellness status, and the insurance policy company you choose.

As soon as you go through the application and medical exam, the life insurance coverage company will examine your application. They need to notify you of whether you've been approved shortly after you apply. Upon approval, you can pay your very first premium and authorize any kind of relevant documents to ensure you're covered. From there, you'll pay your costs on a monthly or annual basis.

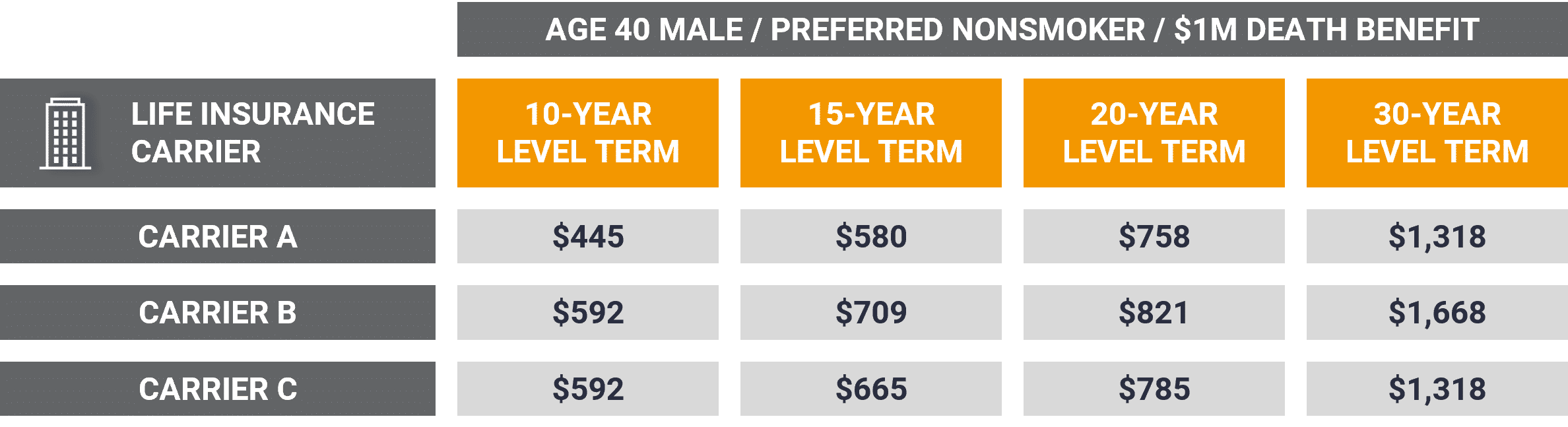

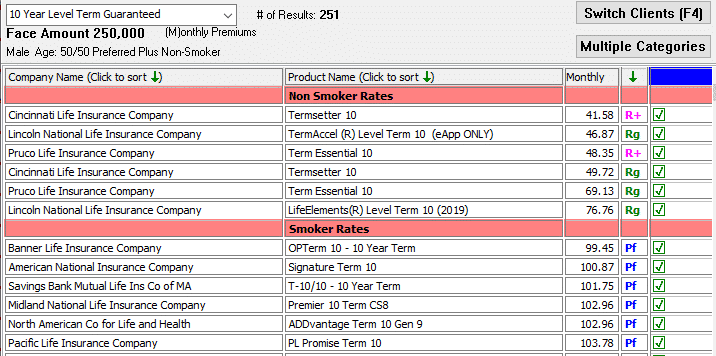

You can pick a 10, 20, or 30 year term and appreciate the added peace of mind you deserve. Functioning with a representative can aid you discover a plan that works ideal for your demands.

As you search for ways to secure your financial future, you have actually likely found a wide range of life insurance coverage choices. a whole life policy option where extended term insurance is selected is called. Selecting the right insurance coverage is a huge choice. You wish to discover something that will help sustain your liked ones or the causes essential to you if something happens to you

Many individuals lean towards term life insurance policy for its simpleness and cost-effectiveness. Level term insurance coverage, however, is a kind of term life insurance policy that has regular payments and an unchanging.

Reliable Term Life Insurance With Accidental Death Benefit

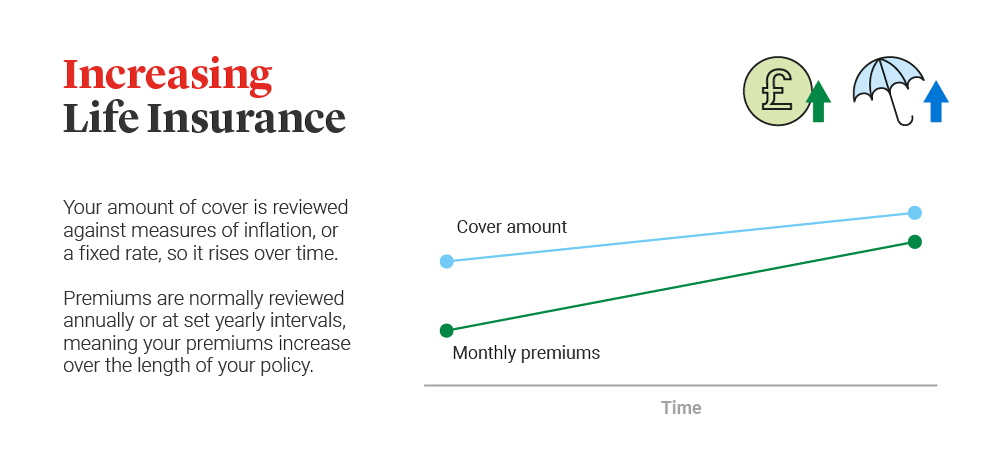

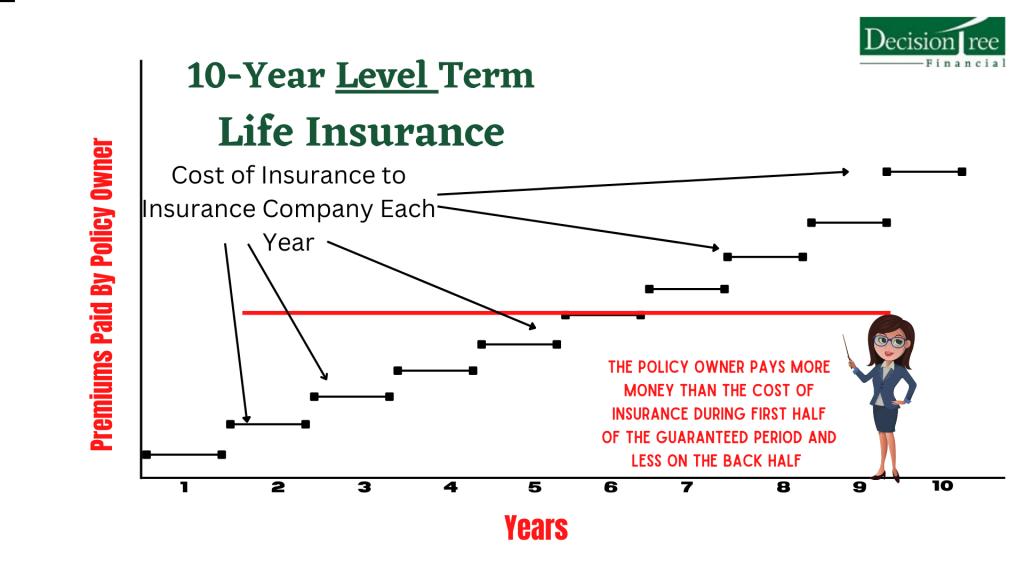

Degree term life insurance policy is a part of It's called "degree" due to the fact that your premiums and the benefit to be paid to your loved ones stay the exact same throughout the contract. You won't see any kind of modifications in price or be left wondering about its worth. Some contracts, such as every year sustainable term, might be structured with costs that raise gradually as the insured ages.

They're figured out at the beginning and continue to be the same. Having constant payments can help you better plan and spending plan since they'll never ever change. Taken care of death advantage. This is likewise set at the beginning, so you can know exactly what survivor benefit amount your can anticipate when you pass away, as long as you're covered and updated on costs.

This typically between 10 and thirty years. You accept a set premium and fatality benefit throughout of the term. If you die while covered, your fatality benefit will be paid to enjoyed ones (as long as your costs are up to date). Your recipients will understand beforehand how a lot they'll get, which can help for preparing purposes and bring them some financial protection.

You might have the choice to for one more term or, a lot more likely, renew it year to year. If your agreement has actually an assured renewability stipulation, you might not need to have a brand-new medical examination to keep your insurance coverage going. Your costs are likely to boost due to the fact that they'll be based on your age at revival time.

With this alternative, you can that will last the rest of your life. In this instance, once more, you may not require to have any type of brand-new medical examinations, however costs likely will increase because of your age and new insurance coverage. a term life insurance policy matures. Different firms provide various alternatives for conversion, make sure to understand your options before taking this action

Dependable Voluntary Term Life Insurance

Speaking to a monetary consultant also may aid you figure out the path that lines up ideal with your general method. Most term life insurance policy is level term for the period of the contract period, however not all. Some term insurance policy may come with a premium that increases over time. With reducing term life insurance policy, your death advantage drops gradually (this kind is often taken out to specifically cover a long-lasting financial debt you're settling).

And if you're established for eco-friendly term life, then your premium likely will rise annually. If you're checking out term life insurance policy and want to ensure straightforward and predictable economic defense for your household, level term might be something to consider. Nevertheless, similar to any type of sort of insurance coverage, it might have some constraints that do not fulfill your needs.

Tailored A Whole Life Policy Option Where Extended Term Insurance Is Selected Is Called

Normally, term life insurance policy is a lot more inexpensive than long-term coverage, so it's an affordable way to protect economic defense. Adaptability. At the end of your agreement's term, you have several choices to continue or proceed from protection, usually without requiring a clinical examination. If your budget or coverage needs change, survivor benefit can be lowered with time and cause a reduced premium.

As with other sort of term life insurance, when the contract ends, you'll likely pay higher premiums for insurance coverage due to the fact that it will certainly recalculate at your existing age and health. Taken care of coverage. Degree term offers predictability. Nonetheless, if your financial circumstance changes, you might not have the necessary protection and may need to acquire additional insurance policy.

That does not mean it's a fit for everybody. As you're buying life insurance, below are a few essential elements to think about: Budget. Among the advantages of degree term coverage is you know the cost and the fatality advantage upfront, making it much easier to without worrying regarding boosts over time.

Age and health. Generally, with life insurance policy, the healthier and younger you are, the extra cost effective the insurance coverage. If you're young and healthy and balanced, it may be an attractive alternative to secure reduced premiums currently. Financial obligation. Your dependents and economic duty play a function in establishing your coverage. If you have a young family members, as an example, level term can help supply financial backing during crucial years without paying for coverage longer than required.

1 All motorcyclists are subject to the terms and conditions of the rider. Some states may differ the terms and conditions.

2 A conversion credit history is not offered for TermOne policies. 3 See Term Conversions section of the Term Series 160 Item Guide for exactly how the term conversion credit is identified. A conversion credit history is not offered if costs or fees for the brand-new policy will certainly be forgoed under the regards to a biker providing disability waiver advantages.

Best Group Term Life Insurance Tax

Term Series items are issued by Equitable Financial Life Insurance Coverage Firm (Equitable Financial) (NY, NY) and are co-distributed by Equitable Network, LLC (Equitable Network Insurance Policy Agency of The Golden State, LLC in CA; Equitable Network Insurance Firm of Utah in UT; and Equitable Network of Puerto Rico, Inc. Term Life Insurance coverage is a type of life insurance coverage policy that covers the insurance holder for a certain quantity of time, which is understood as the term. Terms typically range from 10 to 30 years and rise in 5-year increments, offering level term insurance coverage.

{kind=link}

Latest Posts

Starting A Funeral Insurance Company

50 Plus Funeral Plans

Guarantee Trust Life Final Expense