All Categories

Featured

Table of Contents

When life stops, the bereaved have no selection yet to maintain moving. Practically immediately, households must take care of the overwhelming logistics of death following the loss of a loved one. This can consist of paying expenses, splitting properties, and managing the funeral or cremation. While fatality, like taxes, is inescapable, it does not have to burden those left behind.

Additionally, a full fatality advantage is typically offered unintentional fatality. A changed survivor benefit returns premium frequently at 10% interest if fatality happens in the first 2 years and entails the most unwinded underwriting. The full survivor benefit is frequently attended to unexpected fatality. A lot of sales are carried out in person, and the market trend is to approve a digital or voice trademark, with point-of-sale choices accumulated and taped using a laptop or tablet computer.

To underwrite this service, firms depend on individual health meetings or third-party data such as prescription backgrounds, fraudulence checks, or motor lorry records. Financing tele-interviews and prescription backgrounds can often be made use of to assist the representative finish the application process. Historically firms rely upon telephone meetings to validate or validate disclosure, yet extra lately to enhance consumer experience, companies are depending on the third-party data suggested above and providing instant decisions at the factor of sale without the interview.

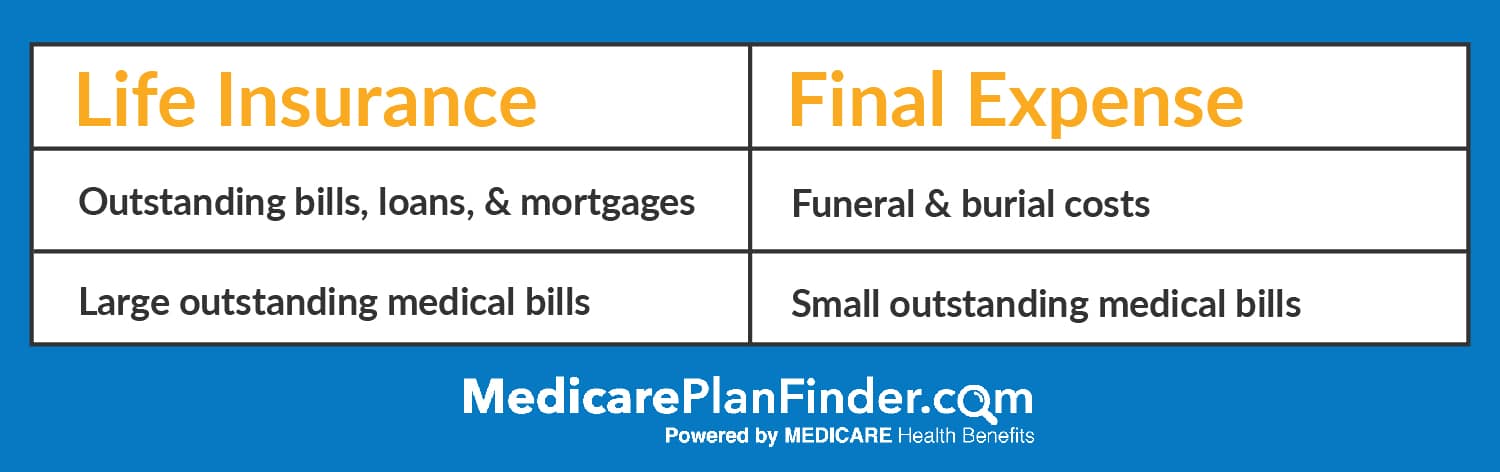

Life Insurance Policy For Burial Expenses

What is last expense insurance, and is it always the ideal course onward? Below, we take an appearance at how final expense insurance policy works and variables to consider prior to you get it.

But while it is referred to as a policy to cover last costs, recipients that receive the survivor benefit are not called for to use it to pay for last expenses they can use it for any type of function they like. That's because last expense insurance policy really drops right into the classification of changed whole life insurance coverage or simplified problem life insurance policy, which are typically entire life policies with smaller death advantages, usually between $2,000 and $20,000.

Connect web links for the items on this page are from partners that compensate us (see our marketer disclosure with our checklist of partners for even more details). Nevertheless, our opinions are our own. See how we rank life insurance policy items to create honest product evaluations. Interment insurance is a life insurance policy plan that covers end-of-life costs.

Funeral Plan Insurance

Burial insurance coverage requires no medical exam, making it accessible to those with medical problems. The loss of a loved one is emotional and distressing. Making funeral preparations and discovering a means to pay for them while grieving adds an additional layer of stress and anxiety. This is where having interment insurance, additionally referred to as last expense insurance, is available in useful.

Streamlined issue life insurance requires a health evaluation. If your health and wellness status invalidates you from conventional life insurance policy, interment insurance might be an alternative.

, interment insurance policy comes in numerous forms. This plan is best for those with light to modest wellness conditions, like high blood stress, diabetes mellitus, or asthma. If you do not desire a medical examination however can qualify for a streamlined concern plan, it is typically a better deal than a guaranteed issue plan due to the fact that you can obtain even more insurance coverage for a cheaper costs.

Pre-need insurance policy is dangerous due to the fact that the beneficiary is the funeral chapel and protection is certain to the selected funeral chapel. Ought to the funeral home fail or you move out of state, you might not have protection, which beats the objective of pre-planning. Furthermore, according to the AARP, the Funeral Consumers Alliance (FCA) recommends against acquiring pre-need.

Those are basically funeral insurance policies. For assured life insurance policy, premium calculations rely on your age, sex, where you live, and insurance coverage quantity. Understand that coverage amounts are restricted and vary by insurance policy supplier. We found sample quotes for a 51-year-woman for $25,000 in coverage living in Illinois: You might choose to opt out of funeral insurance if you can or have actually conserved up sufficient funds to repay your funeral and any type of arrearage.

Burial insurance supplies a simplified application for end-of-life coverage. Most insurer need you to talk to an insurance agent to look for a policy and get a quote. The insurance agents will request for your personal info, contact details, economic information, and protection choices. If you choose to purchase an ensured problem life policy, you won't need to go through a medical test or questionnaire.

The goal of living insurance coverage is to reduce the concern on your loved ones after your loss. If you have an additional funeral service policy, your loved ones can utilize the funeral policy to deal with last costs and get an immediate disbursement from your life insurance coverage to take care of the home loan and education expenses.

People who are middle-aged or older with medical conditions might think about burial insurance coverage, as they could not get conventional policies with stricter approval standards. Furthermore, burial insurance coverage can be handy to those without considerable financial savings or conventional life insurance policy coverage. Interment insurance coverage differs from various other types of insurance in that it uses a reduced survivor benefit, usually only enough to cover expenditures for a funeral and other connected costs.

Selling Final Expense Over The Phone

Information & Globe Record. ExperienceAlani has actually examined life insurance coverage and family pet insurance coverage companies and has composed countless explainers on traveling insurance policy, credit scores, financial debt, and home insurance. She is enthusiastic regarding demystifying the complexities of insurance and various other individual money topics so that viewers have the details they require to make the most effective money choices.

The more insurance coverage you obtain, the greater your premium will be. Final cost life insurance has a number of advantages. Particularly, everyone that applies can get approved, which is not the instance with other kinds of life insurance policy. Last expenditure insurance coverage is typically recommended for senior citizens that might not get traditional life insurance because of their age.

Furthermore, last cost insurance policy is advantageous for individuals who intend to pay for their own funeral. Interment and cremation solutions can be pricey, so final expenditure insurance coverage provides tranquility of mind knowing that your enjoyed ones won't need to utilize their financial savings to pay for your end-of-life plans. Last expense protection is not the best product for every person.

Colonial Penn Final Expense Whole Life Insurance

You can look into Principles' overview to insurance at different ages if you need help deciding what kind of life insurance coverage is best for your phase in life. Obtaining whole life insurance policy through Values is quick and very easy. Protection is available for seniors between the ages of 66-85, and there's no medical examination needed.

Based on your responses, you'll see your approximated price and the amount of coverage you get approved for (between $1,000-$30,000). You can acquire a policy online, and your coverage begins immediately after paying the initial premium. Your rate never transforms, and you are covered for your entire life time, if you continue making the monthly settlements.

When you offer final expense insurance policy, you can give your clients with the peace of mind that comes with knowing they and their families are prepared for the future. Prepared to find out everything you require to understand to begin marketing last expenditure insurance policy successfully?

Additionally, clients for this kind of strategy could have severe legal or criminal histories. It is essential to keep in mind that various carriers offer a variety of problem ages on their assured problem plans as reduced as age 40 or as high as age 80. Some will also use higher stated value, up to $40,000, and others will certainly allow for far better death advantage problems by improving the rate of interest with the return of premium or lessening the variety of years up until a complete fatality advantage is readily available.

{kind=link}

Latest Posts

Starting A Funeral Insurance Company

50 Plus Funeral Plans

Guarantee Trust Life Final Expense